Under the Loan: Lending Trends by Sector

In the scope of our research we have highlighted certain foundational problems in the economy which, against the backdrop of generalized data growth in the economy and exports, show the true state of Armenia’s economy.

We have shown that:

- households have actually become poorer recently,

- from a living perspective Yerevan is even more expensive than Moscow,

- there is currently a capital outflow,

- 75 percent of RA exports is the re-export of gold and diamonds,

- the latter is the only direction providing export growth,

- as well as GDP growth against the backdrop of a decline in the real economy and exports,

- electricity production and export have declined,

- there is a declining trend in tourism and IT services.

In reality the real economy is experiencing a decline.

Against the background of all this, the continuous inflated growth of GDP and export indicators causes quite a bit of concern, against the backdrop of the real economy’s decline. All other conditions being equal, it is expected that Armenia’s 2024 exports will be about 16-18 billion dollars, of which re-exports estimated by our methodology will be about 85 percent (pure exports will amount to about 2.8 billion dollars), compared to 2021 when exports were 3 billion dollars, of which re-exports estimated by our methodology were just 6 percent. In 2023 exports registered a rapid growth. This year 5.4 billion dollars of goods were exported, of which by our assessment re-exports constituted 26 percent. In 2023 exports amounted to 8.4 billion dollars, estimated re-exports at 49 percent or nearly 2 times more. As we noted, it is expected that exports will amount to 16-18 billion dollars in 2024, of which re-exports will be about 85 percent. In fact, at this moment economic growth is conditioned solely by external impulses coming from Russia, and if the re-export of gold from Russia is disrupted or there is a sharp change in the international situation, it will be difficult to secure the growth of Armenia’s overall economic indicators.

In this analysis we will examine certain indicators of monetary policy, which also highlight the problems present in the economy.

Chart 1.

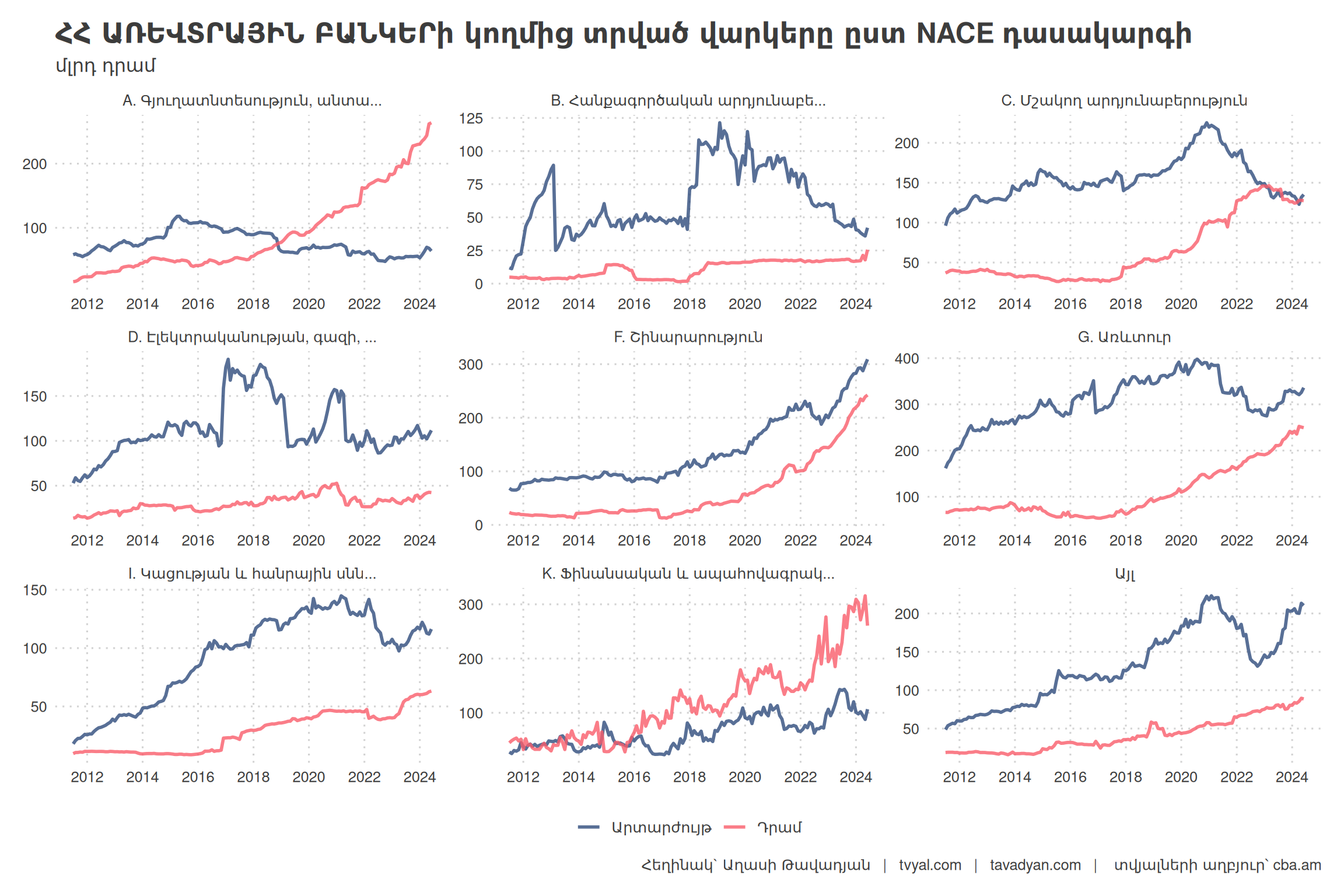

The first chart presents loans provided by commercial banks by sector. As can be seen, loans provided in foreign currency to the industrial sector have had a declining trend since 2021. In December 2020, foreign currency loans equivalent to 484 billion drams were provided to the industrial sector, and in April 2023 it was already 255 billion drams. During this period the decline was 47 percent. Loans provided to this sector in AMD also have a declining trend, which began at the start of 2023. This circumstance testifies that real industry is currently declining. The frightening part is that the main growth of GDP and economic activity recently has been secured precisely by industry, the majority of which is officially conditioned by gold production, which is the result of significant re-exports of precious and semi-precious stones and metals recorded in recent months.

Loans provided in foreign currency to the trade sector also have a declining trend, but this is compensated by loans provided in drams, which is positive. Lending to agriculture, like the trade sector, also has a somewhat positive trend; here foreign currency loans have decreased, while AMD lending has recorded significant growth. Loans provided in drams to the agricultural sector have almost doubled since 2022. Lending to construction is growing in both drams and foreign currency, which also shows a somewhat positive trend. Since 2020 loans provided to this sector in drams have grown by more than 3 times, and in foreign currency by 1.5 times.

Chart 2.

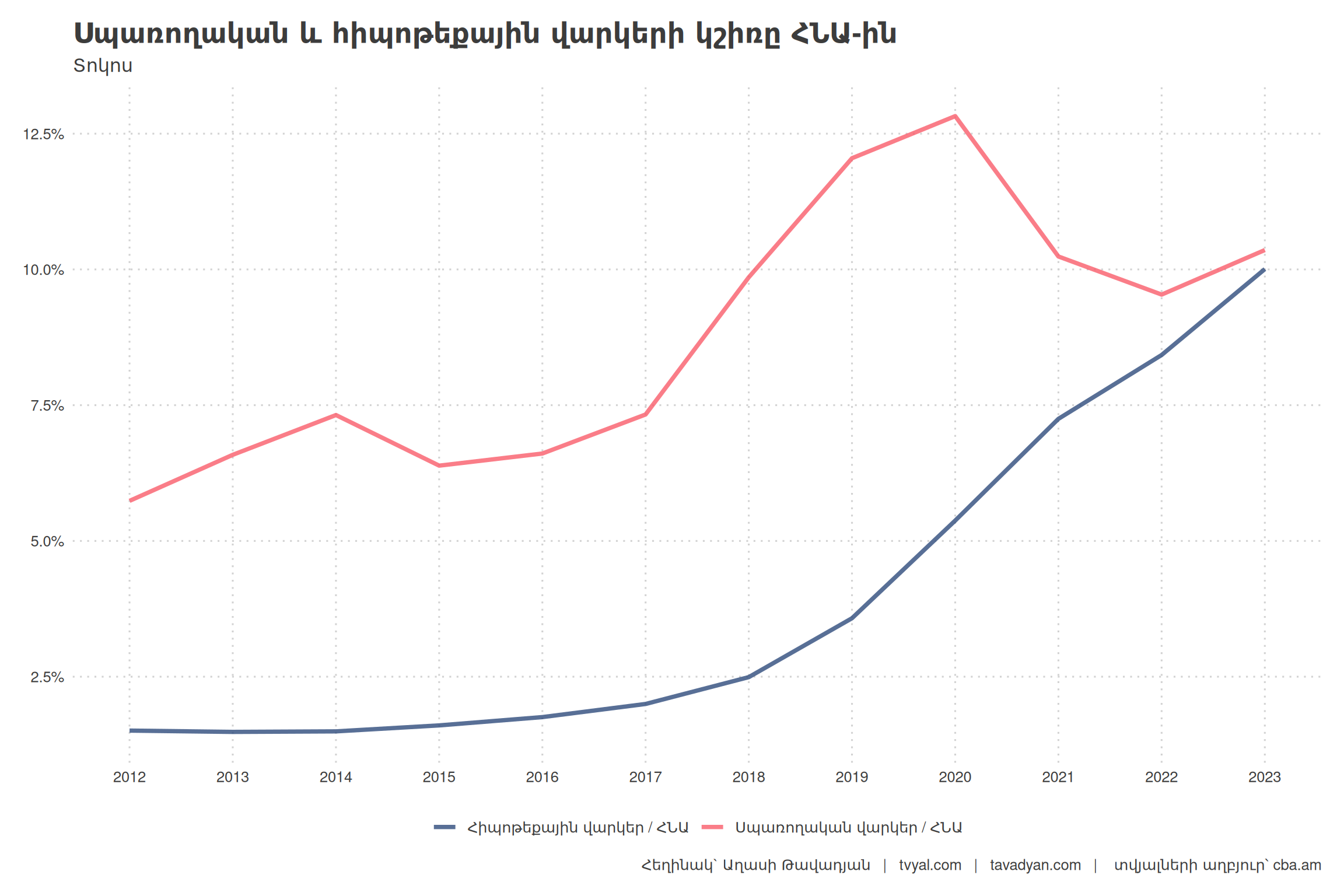

The sharp growth in mortgage and consumer loans recorded recently causes some concern. Mortgage loans provided in AMD as of April 2024 exceeded 1 trillion drams. As of the end of 2023 this indicator was 951 million drams, and GDP was 9505 million drams; thus the ratio of mortgage loans to GDP already constitutes 10 percent and has a clear growth trend, compared to 2018 when the ratio of mortgage loans to GDP was 2.5 percent. As seen in the chart, the ratio of consumer loans to GDP also has a growth trend.

The next chart shows the specific weight of bank loans by sector. In 2018, 20.3 percent of total loans were provided to industry, and 17.1 percent to trade. In 2023 the specific weight of these indicators decreased to 11.8 percent and 13.3 percent respectively. Instead, the specific weight of consumer and mortgage loans grew. In 2018 mortgage loans constituted 10 percent of total loans, and in 2023 already 25 percent. Together these two loans were 37.5 percent of total loans in 2018, and in 2023 already 50.3 percent.

Chart 3.

It is also interesting to examine bank lending by GDP output, according to the classification of economic activity types (NACE Rev.2). As can be seen, at the end of 2023 total loans provided to the economy across different branches amounted to 2.7 trillion drams, which is 11.8 percent higher than the 2.3 trillion dram indicator of 2022. However, as seen in the chart, a lending decline trend is already present. The last time such a decline trend was present was at the beginning of 2021 when total provided loans contracted by 9.2 percent, which was primarily a consequence of the -7.2 percent economic decline of 2020. The same trend has been observed since the beginning of 2024, which also testifies to the fundamental problems present in the economy.

Chart 4.

The trend of decline in total lending is concerning, and it testifies that there is a decrease in lending in the economy, as well as indicating trends of economic contraction. As we have shown in our previous studies, the export growth at this moment is mainly secured by the re-export of gold and diamonds from Russia to the UAE and Hong Kong (almost a 9-fold growth in one year), as well as to some extent the export of textiles and ores. In all other, as well as traditional branches, there is a decline in exports, as well as some decline in lending. This testifies that the 7 percent economic growth planned by the 2024 budget, against the backdrop of an overall real economy decline, can be secured mainly by the continuation of the gold re-export fever from Russia, which is an external factor.

The final chart presents lending to the economy by separate branches.

Chart 5.