The Pendulum of Public Debt: For the First Time, Domestic Debt Exceeds External Debt

For the first time in the structure of the Republic of Armenia’s state debt, the share of domestic debt has exceeded 50 percent. As of May 2024, the government’s state debt amounted to 11 billion 577 million dollars or 4 trillion 496 billion drams, of which 50.2 percent accounts for domestic sources, and 49.8 percent for external sources.

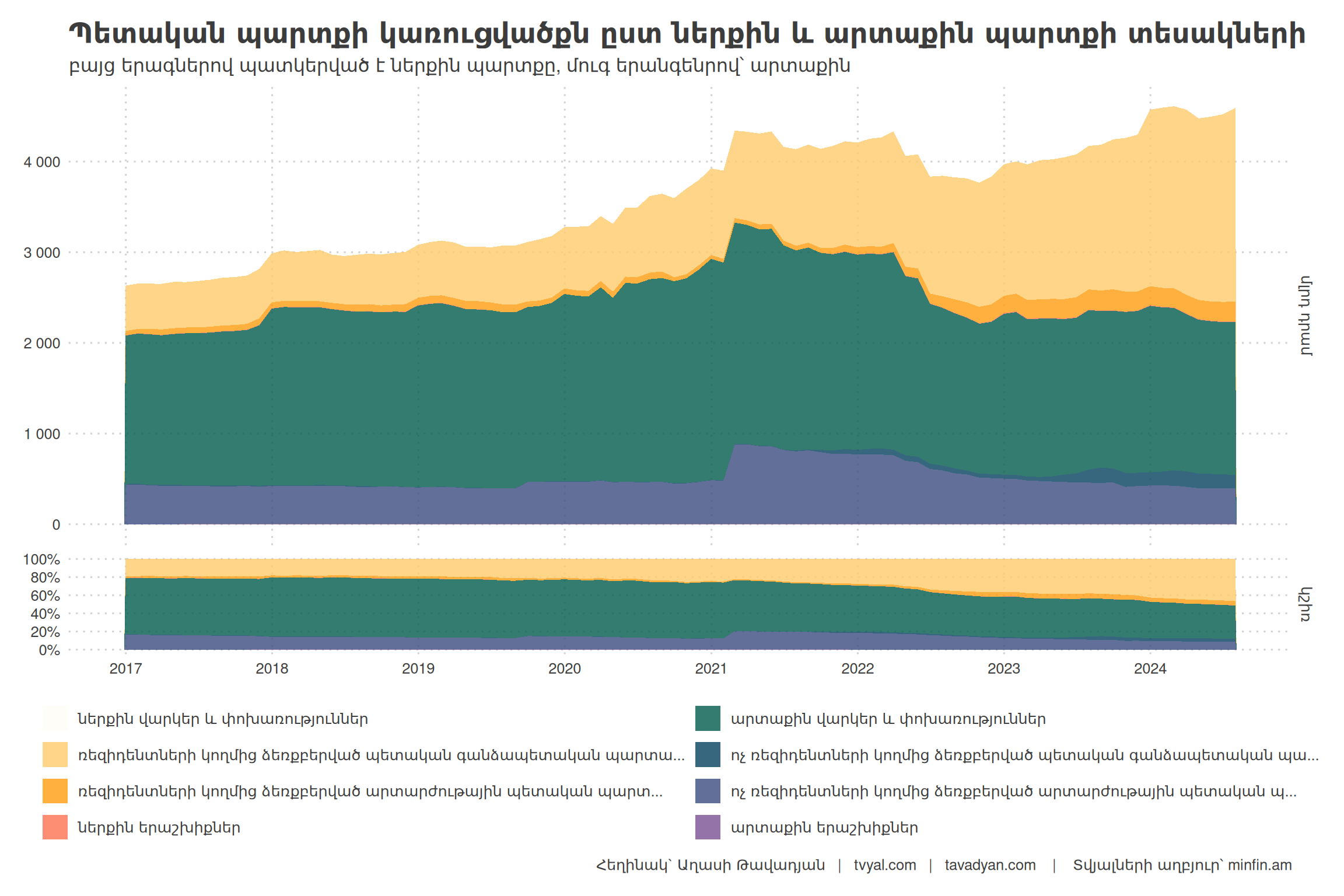

This change marks significant progress compared to 2017 when the Government’s domestic state debt constituted 20.4 percent of the total debt, while the external debt stood at 79.6 percent.

Chart 1.

It should be noted that as of 2017, the Armenian government’s debt was 6 billion 173 million dollars or 2 trillion 988 billion drams. During this period, the state debt has increased by 50.5 percent in drams, and by almost 2 times in dollars at 87.5 percent. This is mainly due to the appreciation of the dram since the beginning of 2017 from 480 drams to 387, which made the servicing of dollar-denominated debt cheaper. In recent years, the policy of increasing domestic debt within the state debt structure has been implemented to curb foreign exchange risks. It should be noted that as of 2023, the state debt to GDP ratio is 48.1 percent, which would cross the 50 percent threshold in the event of a 20-point depreciation of the AMD against the dollar. According to paragraph 63 of the EAEU agreement, the total state debt should not exceed 50 percent of the gross domestic product. According to current fiscal rules, when the Government’s debt exceeds 60% of GDP, the executive is obliged to limit current expenditures, as well as present a program to reduce the level of Government debt relative to GDP. The Ministry of Finance of the Republic of Armenia implements its medium-term policy in such a way as to keep the state debt to GDP ratio within the 50 percent range. Chart 2 presents the structure of state debt by domestic and external debt types:

Chart 2.

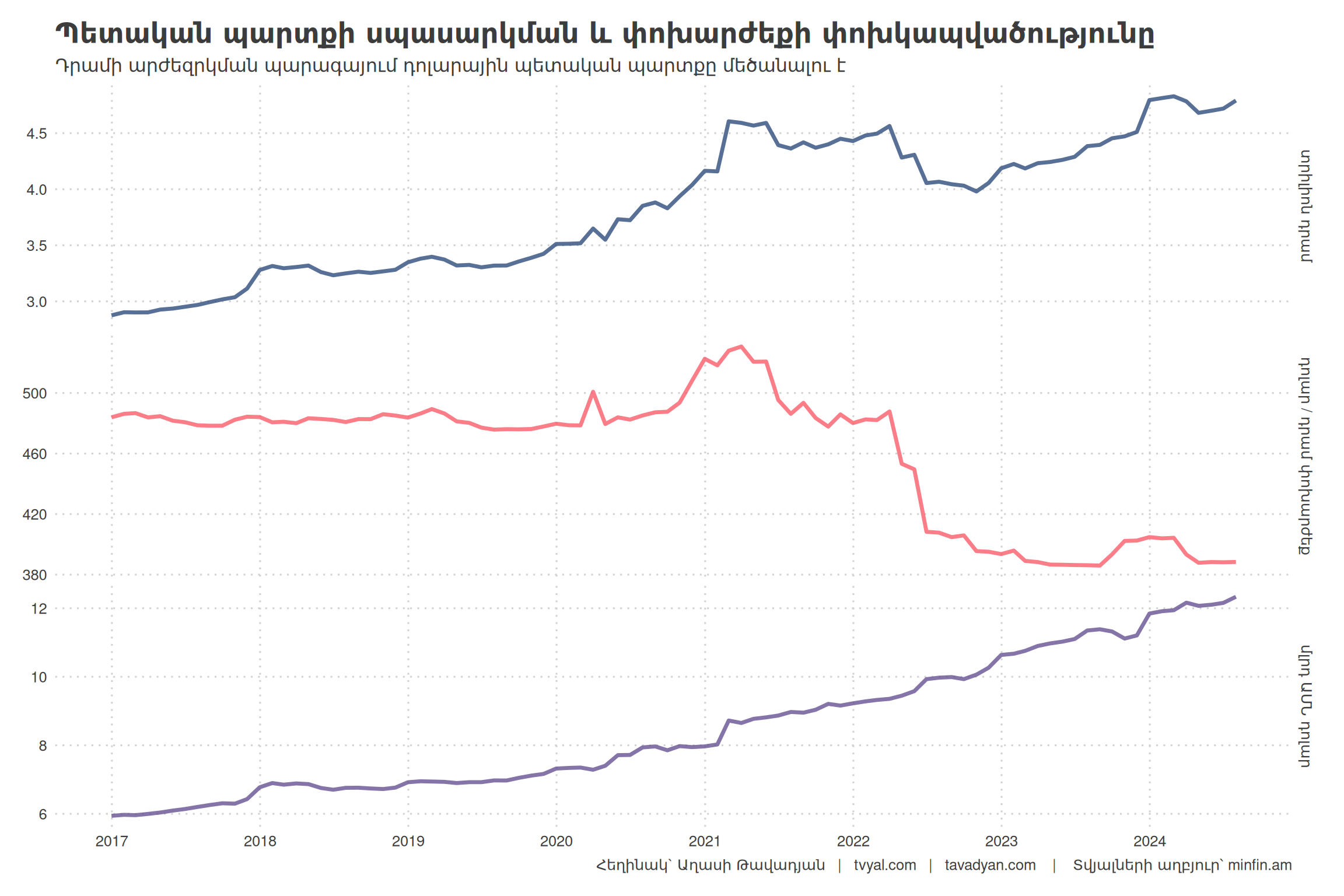

The weighted average interest rate of the Government’s debt has slightly increased, reaching 7.3 percent. This is mainly due to the fact that domestic dram debts, which the state attracts by issuing bonds, carry a higher interest rate. Global crises and abrupt geopolitical changes can lead to an increase in the state debt to GDP ratio, and the policy of increasing domestic state debt restrains external risks. 49.0 percent of the Government’s debt is in drams, 29.9 percent in dollars, 9.1 percent in euros, and the rest in other currencies. The increase in domestic debt reduces external financial risks. Chart 3 shows the correlation between state debt service and the exchange rate:

Chart 3.

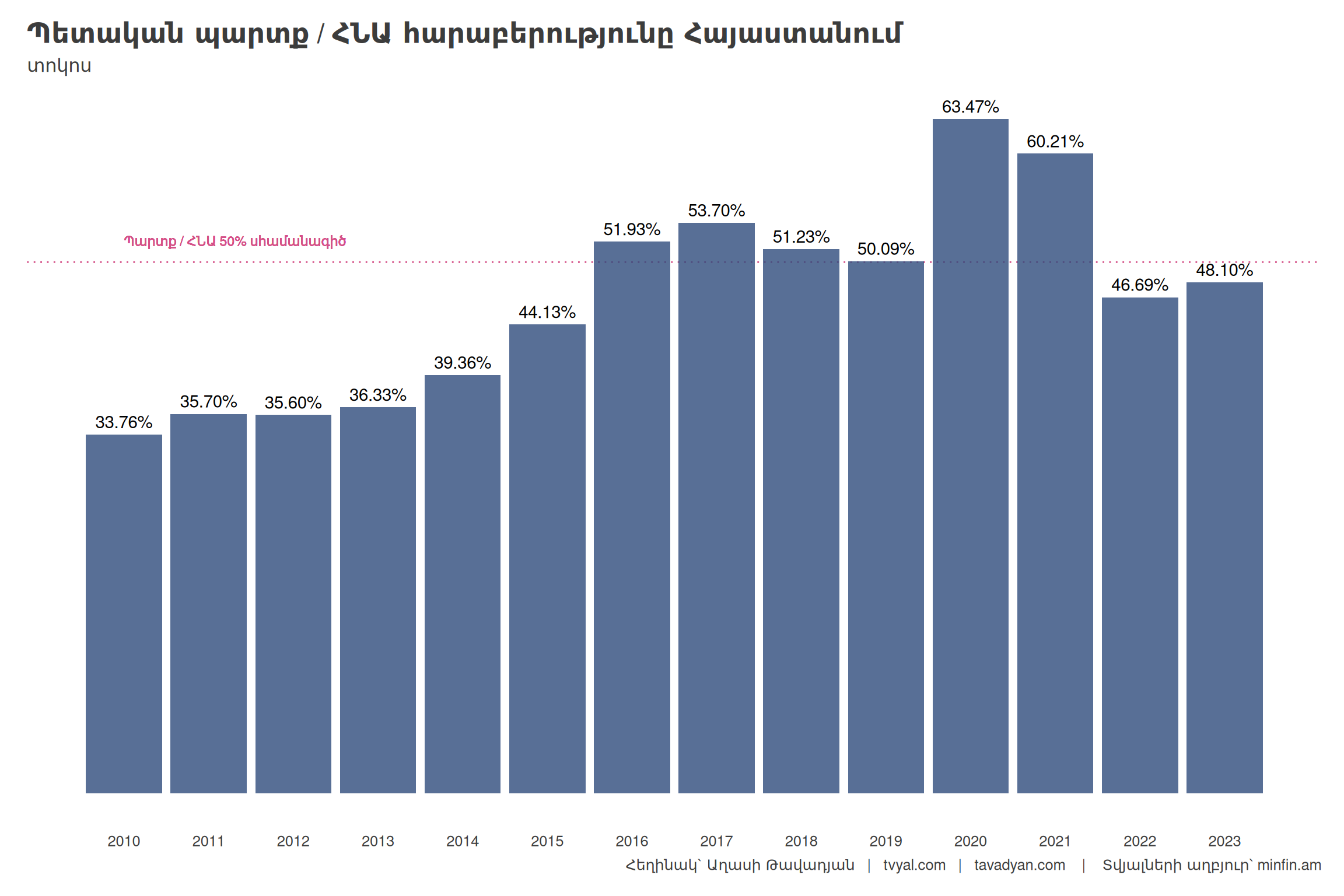

As seen in Chart 4, the state debt to GDP ratio crossed the 50 percent threshold for the first time in 2016, amounting to 51.9 percent. This was primarily due to the currency crisis in Russia, as a result of which all currencies in the region depreciated, including the dram, which sharply increased the servicing cost of the external state debt. On an annual basis, the state debt to GDP ratio reached its peak in 2020 when it crossed the 63.5 percent boundary, and on a quarterly basis, it reached 69.8 percent in the first quarter of 2021. It should be noted that GDP growth in 2020 was negative, amounting to -7.2 percent. This was mainly due to anti-epidemic measures and the 44-day war, which also contributed to the growth of the state debt. In 2022, the state debt to GDP ratio was largely able to decrease at the expense of dram appreciation. This was due to the fact that in 2022, driven by sanctions against Russia, a fairly large amount of foreign currency entered Armenia. This appreciated the dram and, as a result, lowered state debt servicing. This situation shows that external factors can have a significant impact on the dynamics of Armenia’s economy and state debt. However, it should be noted that such situations cannot be considered a stable trend, and in the long term, attention must be paid to developing more sustainable mechanisms for state debt management.

Chart 4.

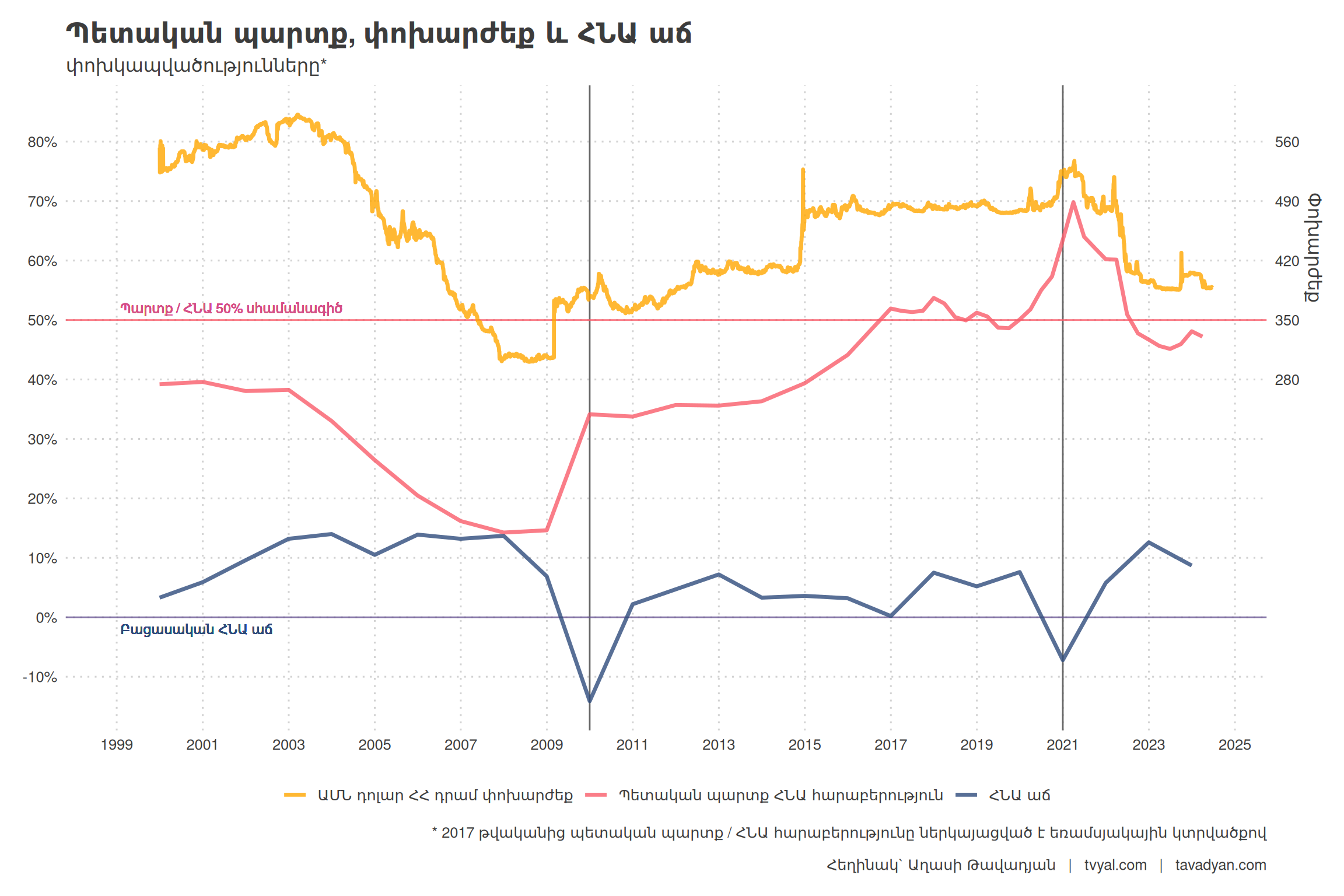

The last chart clearly shows the impact of the dollar exchange rate on state debt servicing and, consequently, on the state debt to GDP ratio. The more the dram appreciates against the dollar, the cheaper state debt servicing becomes, therefore the state debt to GDP ratio decreases. Conversely, the more the dram depreciates, the more the state debt to GDP ratio tends to grow. It is worth noting that the Armenian dram has been the most appreciated among convertible currencies since 2020, which negatively affects real exports, as well as tourism and the IT sector. This exerts some pressure on the dram, which is de facto softly pegged to the dollar. The depreciation of the dram will negatively affect state debt servicing and, as a secondary consequence, GDP growth. The chart also shows the inverse correlation between state debt and GDP growth. In the case of negative GDP growth, state debt grows sharply because the target set by the state budget is not met. As a result, the budget reserve fund is forcedly consumed, and subsequently, the state debt also grows. This trend can be seen in the last chart in 2010, following an average economic growth of 12 percent between 2002 and 2008. This decline was due to the Global Financial Crisis. A similar situation was also observed in 2020: the economic downturn this time was due to another global phenomenon, the COVID-19 pandemic. As a result, both crises increased the state debt to GDP ratio. In other words, the dram exchange rate has a direct impact on state debt growth, while GDP growth has an inverse impact. Over the last 25 years, negative GDP growth has mainly been due to global “black swan” events. Chart 5.

This analysis shows that Armenia’s economy is sensitive to global shocks, and state debt management requires a cautious approach that takes into account the potential impact of external factors.

Overall, it is welcome and encouraging that the share of domestic debt in the state debt structure has crossed the 50 percent threshold for the first time, as well as the fact that the predominant currency in the state debt is the Armenian dram. However, starting from 2022, the dram has been the most appreciated among convertible currencies, which has a negative impact on real exports, as well as on tourism and the export of IT products. This, in turn, can negatively affect the prospect of 7 percent economic growth envisaged by the 2024 budget law. Currently, there are key problems in the economy. It should be noted that both further depreciation of the Armenian dram and a decline in GDP can negatively affect state debt servicing, in which case the state debt to GDP ratio could cross the 50 percent threshold. Conclusion

This analysis shows that Armenia’s state debt management policy has undergone significant changes in recent years. The growth of the domestic debt share and the predominance of debt in drams are positive trends that contribute to the reduction of foreign exchange risks. But at the same time, a number of challenges must be taken into account:

- The potential impact of dram depreciation on the ratio of state debt and GDP.

- The vulnerability of Armenia’s economy to global economic shocks.

- The negative impact of dram appreciation on exports, tourism, and IT sectors.

In this situation, it is necessary to continue a cautious and balanced state debt management policy, while paying attention to the development of the real sector of the economy and maintaining external competitiveness.

limit.

- 🎯 What caused the recent fluctuations of the ruble?

- 🎯 What percentage of Russian gold passes through Armenia?

- 🎯 What key problems are there in Armenia’s economy?

- 🎯 What will leaving the EAEU give to Armenia’s economy?