Armenia: Caucasian Tiger or Expensive Dream?

The Illusion of Armenia’s Economic Growth

Armenia’s economy is standing at a turning point. Recent revisions to GDP growth have revealed a concerning reality: the country’s economic surge, which was heavily praised recently, was primarily built on unsustainable factors. Upon carefully examining the data, it becomes clear that economic growth is an illusion: the reality presents serious challenges.

GDP Growth: The History of Revision

The Illusion of Prosperity

Following the latest revision, GDP growth indicators were downgraded by 2.6 percentage points. These reductions sent shockwaves through the Armenian economic sphere, forcing a reassessment of the country’s economic health.

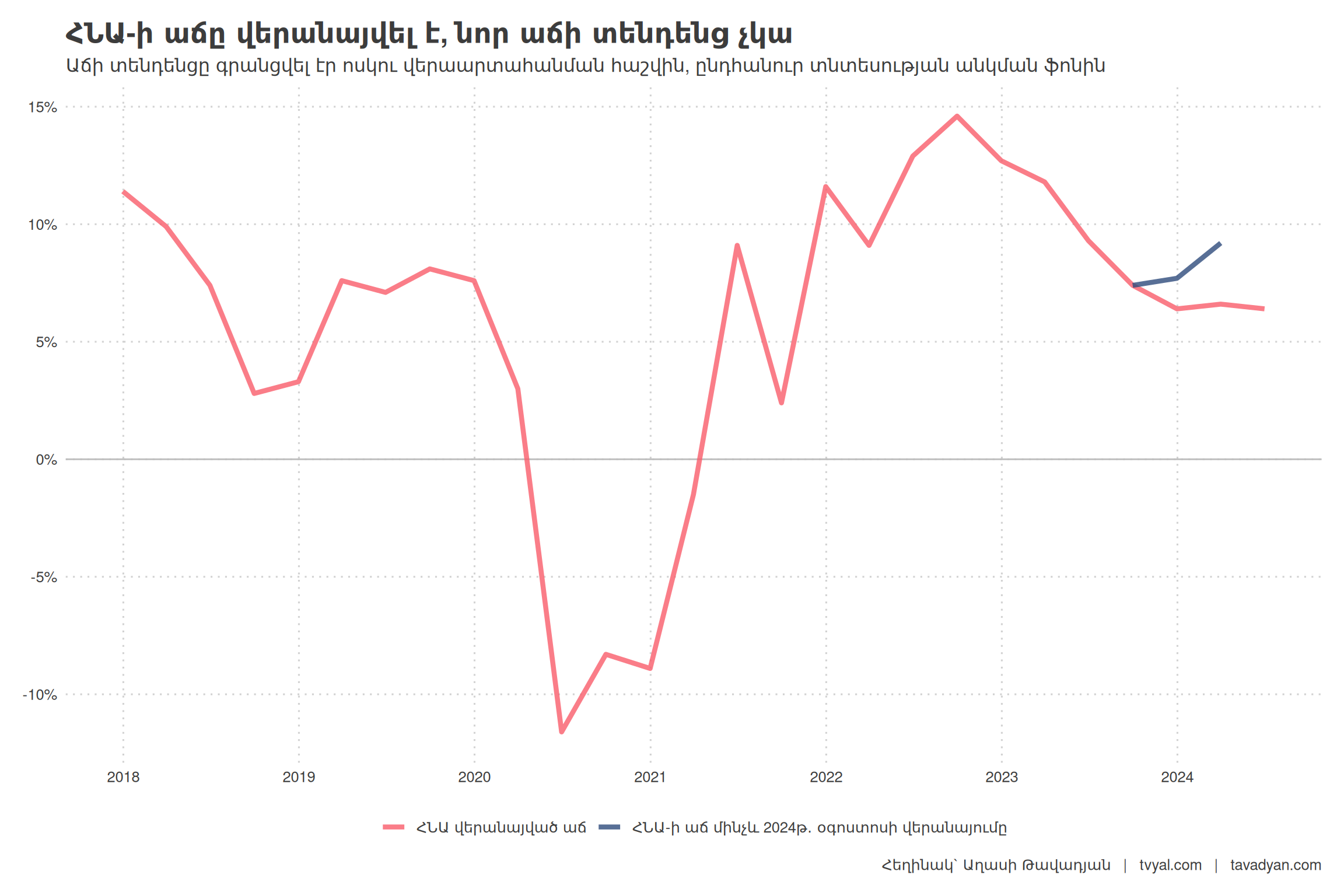

Chart 1.

The first chart shows the volatility of Armenia’s economic trajectory. While the long-term average growth hovers around 4.5%, significant fluctuations have been observed in recent years. Recent revisions bring these numbers closer to the historical average, calling into question the sustainability of the recent growth.

Unveiling the Illusion of Growth

The story behind the revision is dramatic and carries far-reaching consequences:

- Growth for the first quarter of 2024 was revised downwards from 9.2% to 6.6%, a significant drop of 2.6 percentage points.

- Growth for the fourth quarter of 2023 was adjusted from 7.7% to 6.4%, a decrease of 1.3 percentage points.

These are not minor adjustments, but a fundamental reassessment of Armenia’s economic reality. As depicted in the chart, prior to this revision the economy appeared to be on an upward trend; after the revision, it showed a clear tendency toward stagnation.

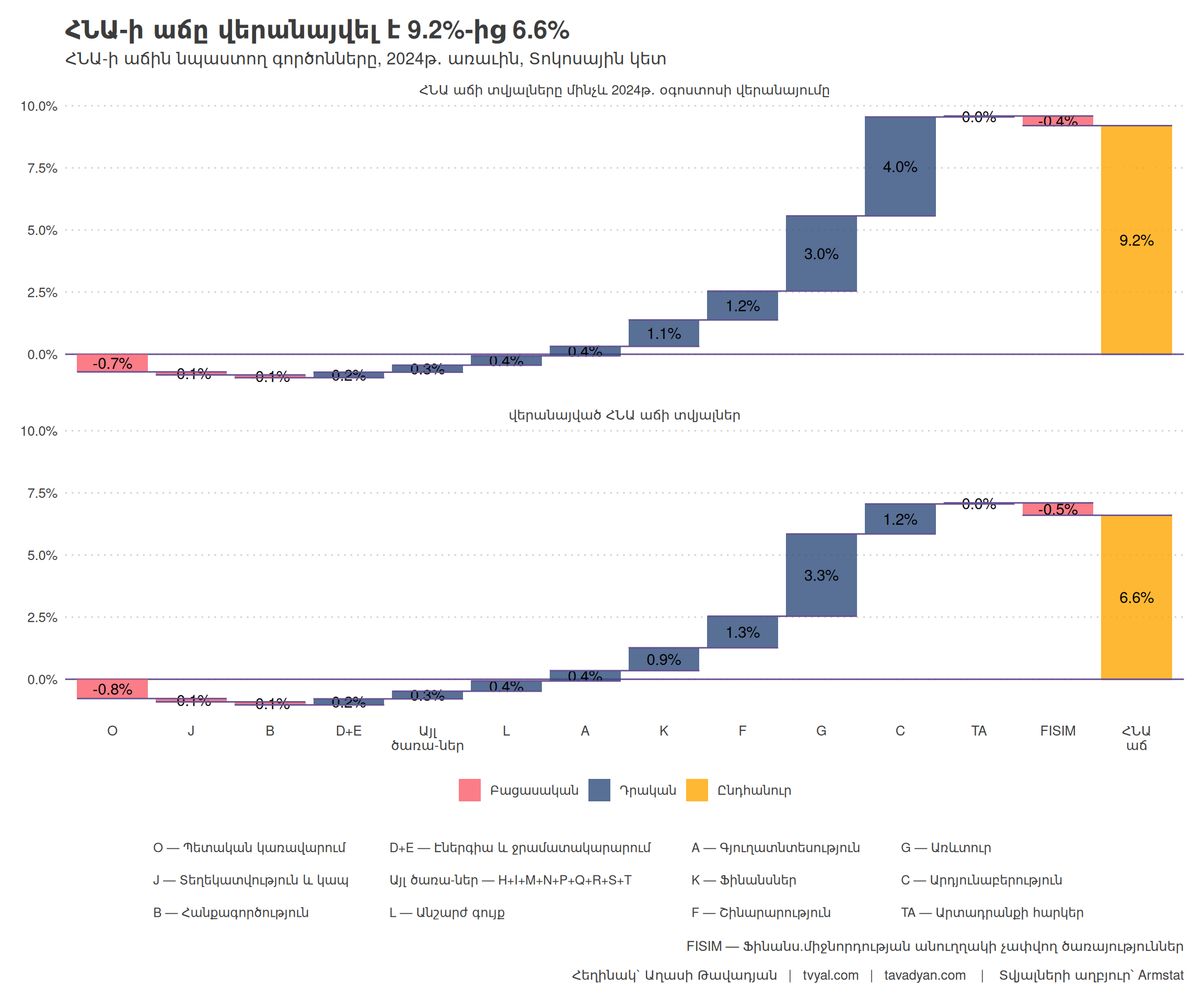

Chart 2.

The second chart illustrates the significant difference “before and after” the GDP growth revision. The industrial sector (C), once considered the driver of growth by providing 4.0 percentage points to the Q1 2024 GDP growth, now contributes a mere 1.2 points. This shocking adjustment exposes the vulnerability of Armenia’s recent growth.

It is worth noting that these figures were revised after we published a report noting that 4% of the value added from gold re-exports, which was questionably paid to the state budget, accounted for 4 percentage points of the 9.2% growth in the first quarter of 2024. It is alarming that the gold re-export “industry” contributed 4%, trade 3%, and financial services 1.1%, while the rest of the economy registered a decline of -0.1%.

Following this post:

- Q1 2024 GDP growth was revised from 9.2% down to 6.6%.

- Industry’s contribution to GDP dropped sharply from 4 percentage points to 1.2.

- The reason: the revision of the indicators of the gold re-export “industry”.

The Precious Effect: The Illusion of Gold Re-exports

At the heart of this statistical drama is the phenomenon of gold re-exports, which gathered momentum from November 2023 and continued through May 2024. This sector imparted a seeming vitality to Armenia’s growth figures. However, recent revisions have effectively zeroed out its contribution to GDP growth.

It should be noted that the 2023 annual economic growth figure is still listed at the 8.7% level and has not yet been revised. In late 2023, we projected that economic growth would be around 7%. However, a significant increase in gold re-exports beginning in November inflated economic growth to 8.7% against a backdrop of overall economic decline, causing a “precious effect”. It can be expected that the 2023 annual economic growth of 8.7% might also be revised down to 7.5%.

Economic Sectors and Their Contribution

Overview of Sector Performance

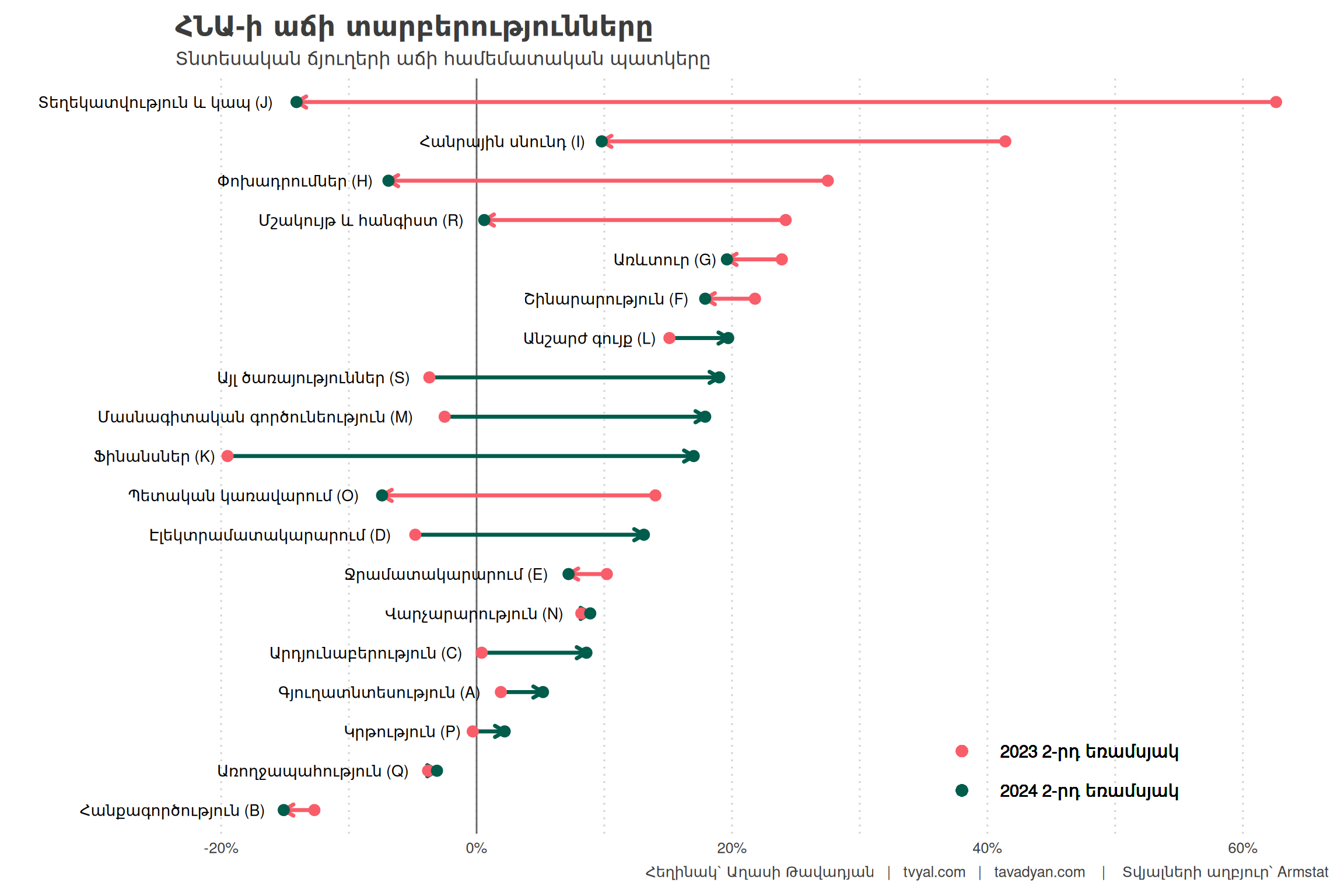

Chart 3.

The third chart shows substantial differences in growth rates among various sectors, indicating that economic growth is neither evenly distributed nor sustainable.

Key observations:

- The IT sector (J), which was one of the growth engines from early 2022 and registered a 62.6% year-on-year growth in Q2 2023, has now experienced a significant decline. In Q2 2024, it showed a 14.1% year-on-year decline.

- Other sectors, including food services (I) and transportation (H), are also experiencing declines.

- Growth in the economy’s main drivers, construction (F) and trade (G), is slowing down.

The Decline of the IT Sector and its Consequences

The decline of the IT sector is particularly concerning. After registering declines for three consecutive quarters, this strategic sector no longer contributes positively to GDP growth. This trend calls into question the sustainability of Armenia’s technology-driven growth strategy and the reasons for this reversal. This points to a crisis within the sector. Read more in our analysis on IT: 🆘🇦🇲🧑🏼💻 SOS Armenian IT: Armenia’s IT sector, from strategic priority to potential decline

Current Drivers of Growth

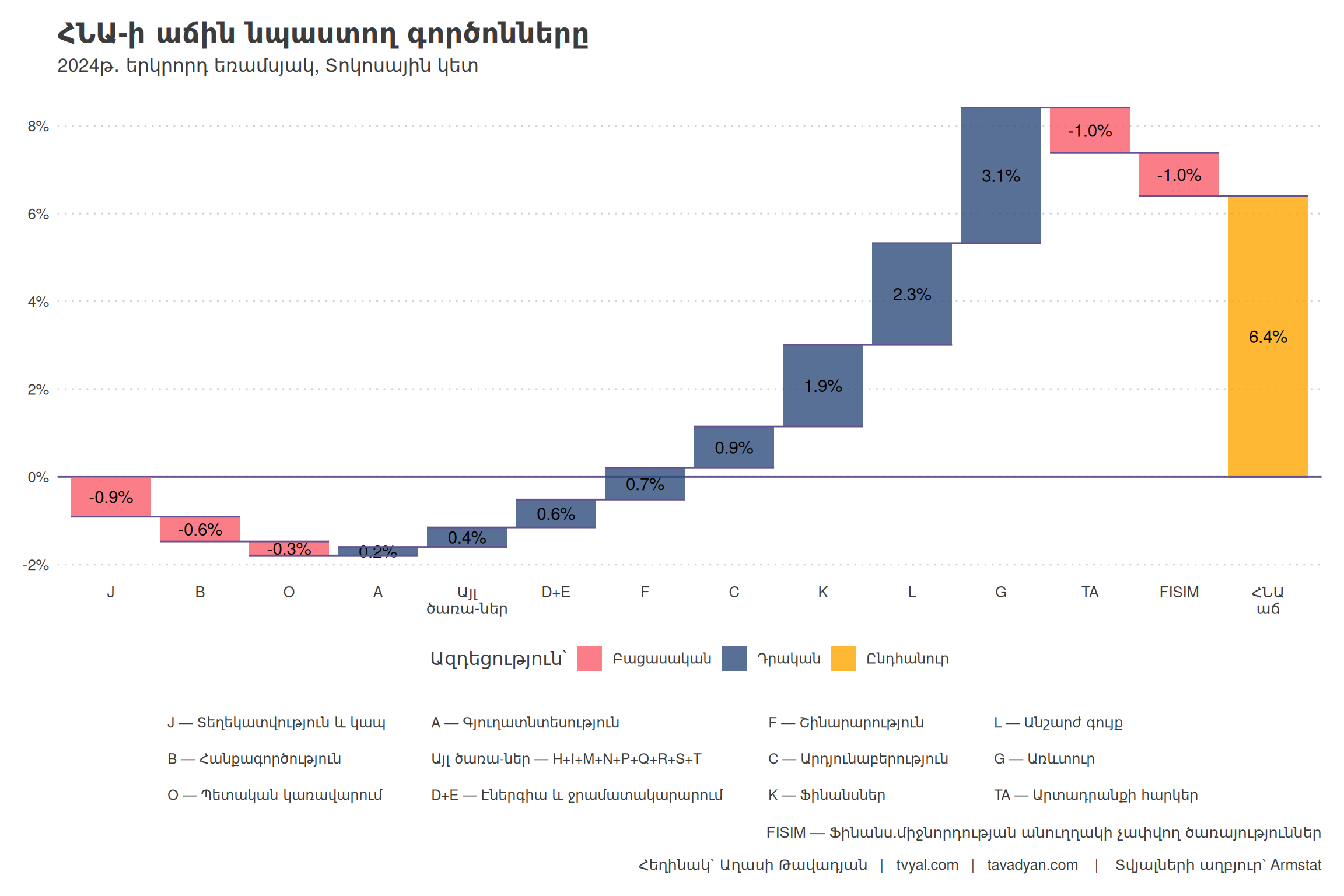

Chart 4.

Chart 4 shows the factors contributing to GDP growth in the second quarter of 2024:

- Wholesale and retail trade (G) provides 3.1 percentage points of the 6.4% GDP growth, almost half.

- Real estate activities (L) provide 2.3 percentage points, about a third of the growth. This is a significant increase compared to the historically recorded average contribution of 0.5 percentage points.

- The financial sector (K) contributes 1.9 percentage points.

The substantial contribution of real estate operations is noteworthy. It includes the “imputed rental value of owner-occupied dwellings”, essentially estimating the potential rent of all apartments in Armenia regardless of whether they are owner-occupied or rented. This means that about one-third of the 6.4% growth is attributed to the increase in the market value of real estate, which may not be sustainable.

Sustainability of Economic Growth

Recent GDP revisions and sector analyses raise serious questions about the sustainability of Armenia’s economic growth.

Analysis of Growth Drivers

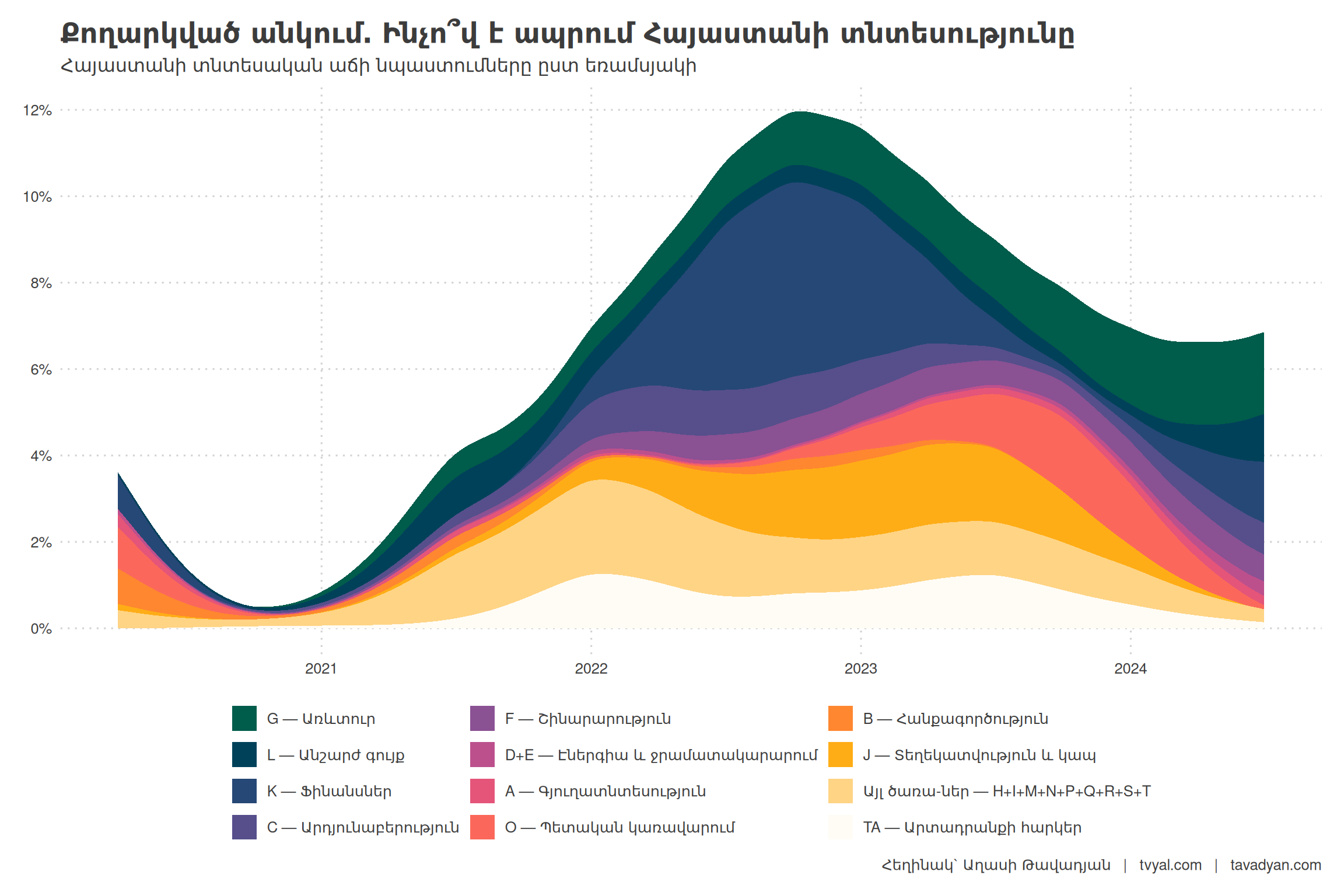

Chart 5.

Chart 5 illustrates the factors contributing to Armenia’s economic growth by quarter. Several important points emerge:

- Long-term average growth: Armenia’s long-term average economic growth rate is about 4.5%. Any system tends to return to its long-term average unless there are qualitative changes within that system capable of generating sustained, long-term value-added growth.

- Post-pandemic recovery: Following the COVID-19 pandemic in 2020 and the 44-day war, the economy showed signs of recovery. Key economic sectors contributed about 4.5% to economic growth.

- IT sector contribution: The IT sector (J) provided about 1-2.5 percentage points of growth, mainly due to the relocation of IT professionals from Russia. However, this sector has been in decline over the last three quarters.

- Financial services and trade: Since early 2022, the bulk of GDP growth was driven by financial services (K) and trade (G). It is noteworthy that as a result of a large capital inflow from Russia, the banking system’s net profit tripled in 2022 (Read more: 💸🔚🏦 Capital Outflow).

- Recent trends: From early 2022 to mid-2023, the main economic sectors showed a stable contribution to economic growth. Since then, however, almost all economic activity classifiers have been registering a decline in their contribution to overall economic growth.

Dependence on Temporary and Artificial Factors

The data indicates that Armenia’s economic growth has been heavily dependent on external factors:

- In 2022, there was a significant capital inflow from Russia.

- Large-scale gold re-exports starting in November 2023 boosted growth indicators (more: 🇷🇺💰🇦🇲 Armenia: A Haven for Russian Gold).

- Growth is mainly driven by trade, real estate, and financial services, which are dependent on external factors (more: 🌅🏖🌄 Beyond the Border: Armenia’s Tourist Surge and Potential Decline).

These factors, while providing a short-term stimulus, do not represent sustainable, long-term drivers of economic growth. Under these conditions, economic growth will gravitate towards its long-term average.

Fiscal Consequences

Issues related to the sustainability of economic growth have a direct impact on Armenia’s fiscal situation.

Challenges in Tax Revenue Collection

Currently, there is a significant tax revenue shortfall of 9%. This deficit leads to discussions about potential cuts in budgetary expenditures (Read more: 🧮⏳🎲 Armenia Taxes Time: A Game with Economic Growth).

Budgetary Expenditure Considerations

Plans are being discussed to use about 150 billion drams from the reserve fund to cover expenses amidst revenue shortfalls. This situation increases the likelihood of a rise in state debt.

Potential Growth in Public Debt

Several factors contribute to the risk of state debt growth:

- If the 7% economic growth stipulated by the budget law is not achieved, and instead the long-term average of 4.5% materializes, the government may be forced to allocate about half of the reserve fund to cover the difference.

- In the case of an economic growth rate of 2.5% or lower, we may be forced to increase the state debt.

- Current positive long-term GDP growth forecasts lack a solid foundation for sustainable, long-term growth in value added.

Conclusion

Recent GDP revisions and sector analyses present a concerning picture for Armenia’s economic future. The heavy reliance of the Armenian economy on external factors and temporary stimuli from activities like gold re-exports indicate that without significant structural changes, maintaining high growth rates will be difficult.

The decline of the IT sector, the unsustainable nature of real estate’s contribution to GDP, and potential fiscal challenges all point to an economy at a crossroads. The risk of public debt growth and possible fiscal instability in the coming years cannot be ignored. 💰🚧⚖️ The Pendulum of Public Debt: For the First Time, Domestic Debt Exceeds External Debt

At present, our long-term forecasts for GDP growth are not positive. Without a solid foundation for sustainable, long-term value-added growth, Armenia may find itself chasing economic illusions rather than building sustainable prosperity (more: 🌿🤨💎 The Precious Effect: Reasons for Economic Growth in 2024). The coming months and years will be crucial in determining whether the country can steer towards more sustainable economic strategies or will continue to rely on unstable and temporary growth factors.