The Public Debt Pendulum: Why is Armenia Borrowing to Pay Off Debt?

Why is Armenia borrowing to pay off debt?

$750 million in new debt, at a high interest rate

On March 12, Armenia issued $750 million in Eurobonds on the international market at a 7.1% interest rate. This number speaks volumes: the interest rate is high, which means foreign investors assess the riskiness of Armenia’s economy as high. But why is the state taking on new debt when the authorities often claim that our economy is growing by “leaps and bounds”? The reason is simple: there is a large gap in the budget. In 2024, tax revenues were 8% less than planned. Such a situation has not existed under the last 3 governments. VAT revenues mainly decreased, meaning that either trade in the country shrank, or it returned to the shadow economy. As a result, Armenia is borrowing to pay off debts. This approach is similar to a family that, instead of cutting expenses, takes out a new loan to pay off the debt of an old loan.

Recently, members of the government and representatives of the Ministry of Economy have demonstrated an incomplete understanding of public debt. The purpose of this article is to present the pros and cons of public debt, which we hope will bring some clarity to this topic.

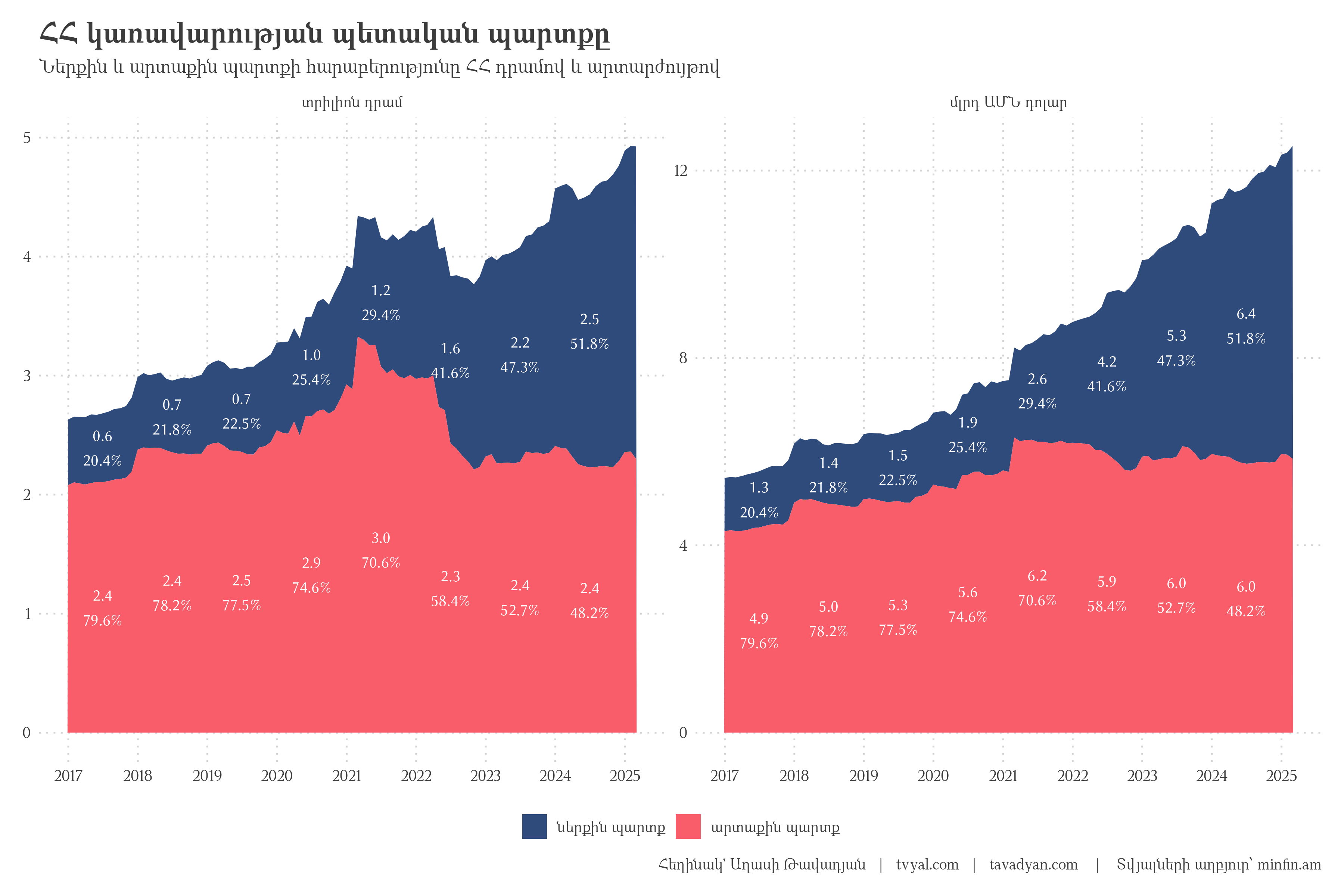

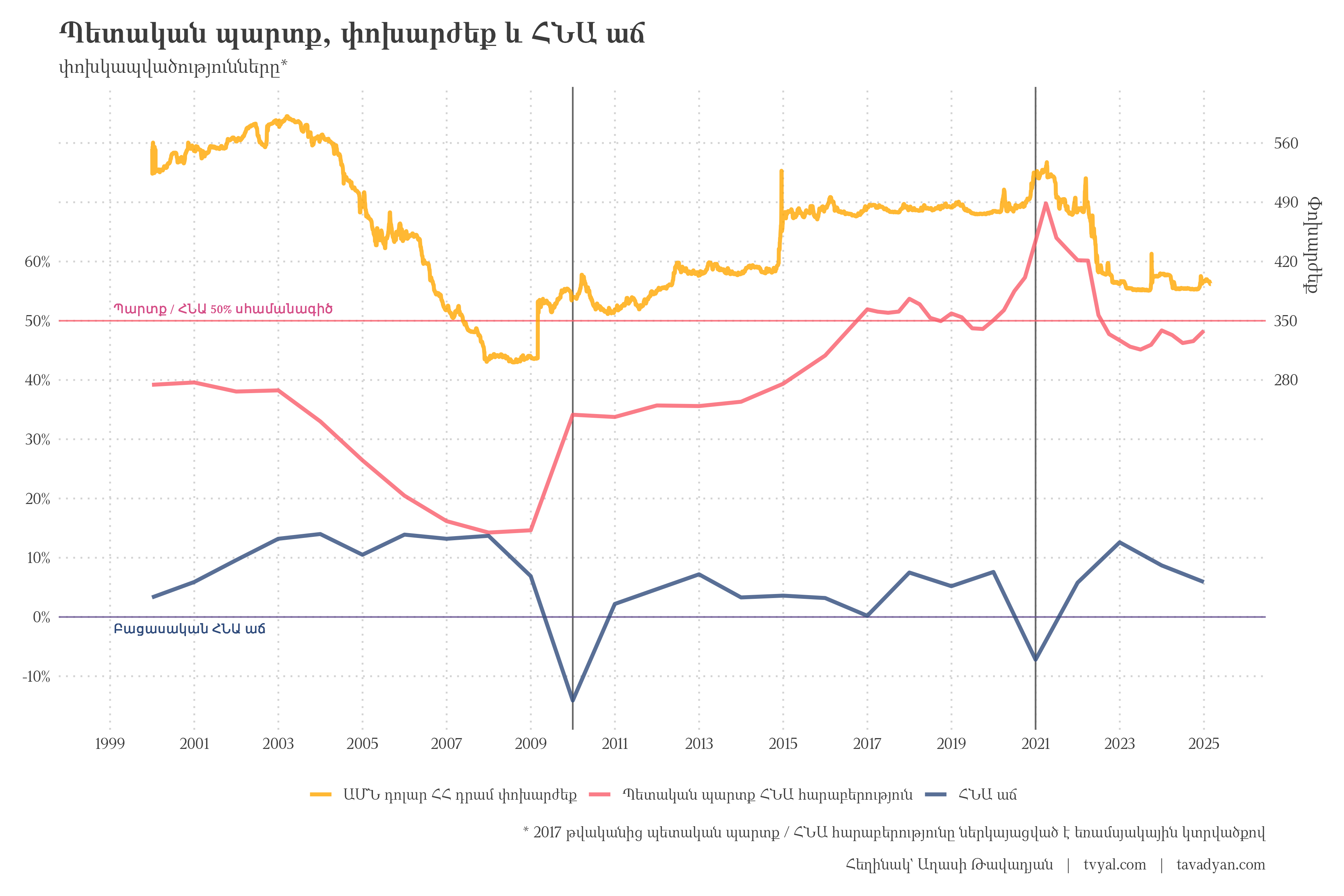

Obvious success: for the first time, internal debt is greater than external debt

Chart 1.

There is also good news for the economy. In the structure of Armenia’s public debt, for the first time, the weight of internal debt exceeded 50%. In numbers, out of the total $12.5 billion (or 4.9 trillion drams) debt, 50.2% is already internal debt, and the remaining 49.8% is external. This change is truly significant if we consider that back in 2017, internal debt was only 20.4%. At the same time, it is alarming that compared to 2018, our public debt has almost doubled, reaching $12.5 billion from $6.4 billion.

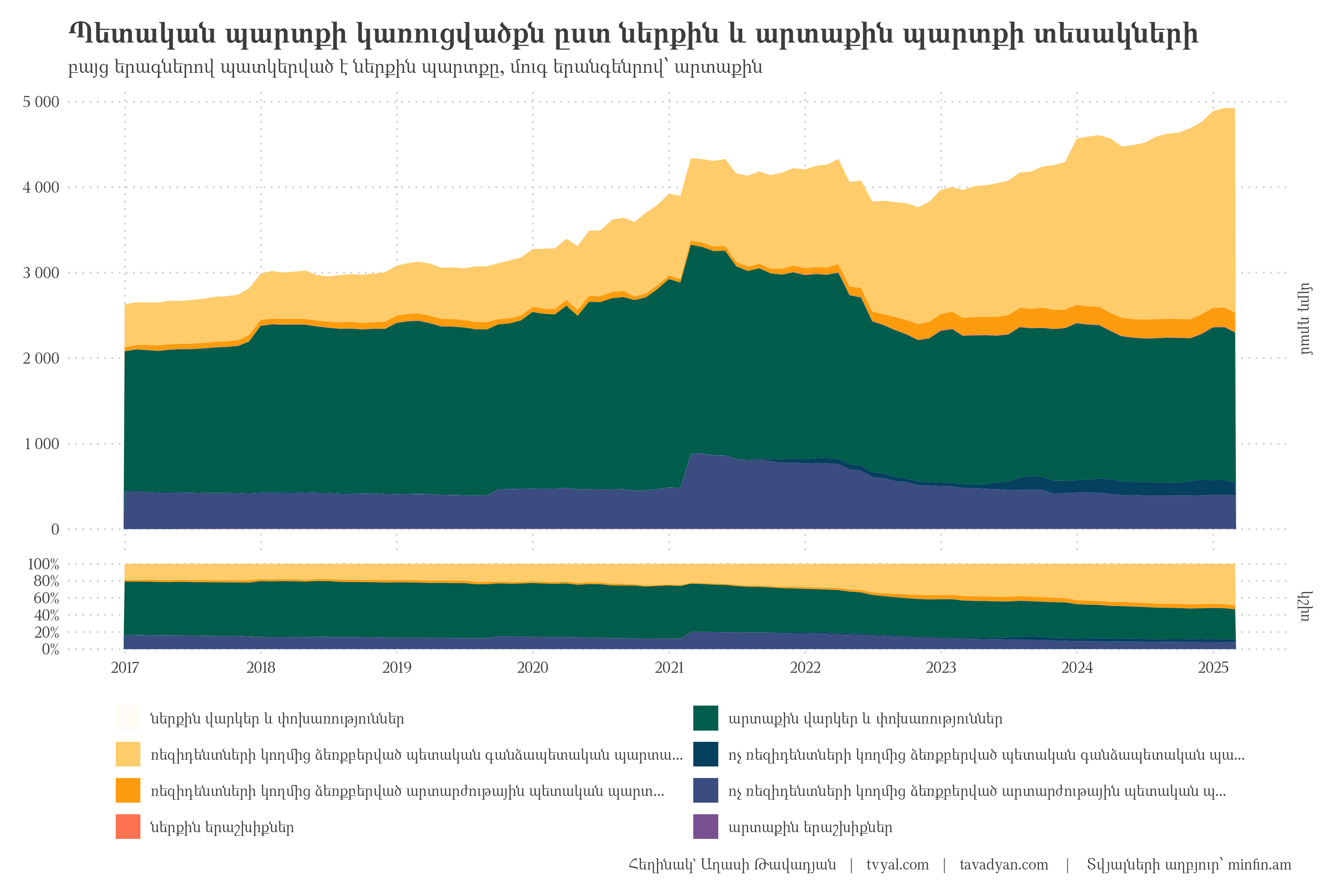

Chart 2.

Currently, 49% of the government debt is in drams, 29.9% in dollars, 9.1% in euros, and the rest in other currencies. This shift is positive because it reduces foreign exchange risks, but it comes with a price: servicing the dram debt is more expensive because its interest rates are higher.

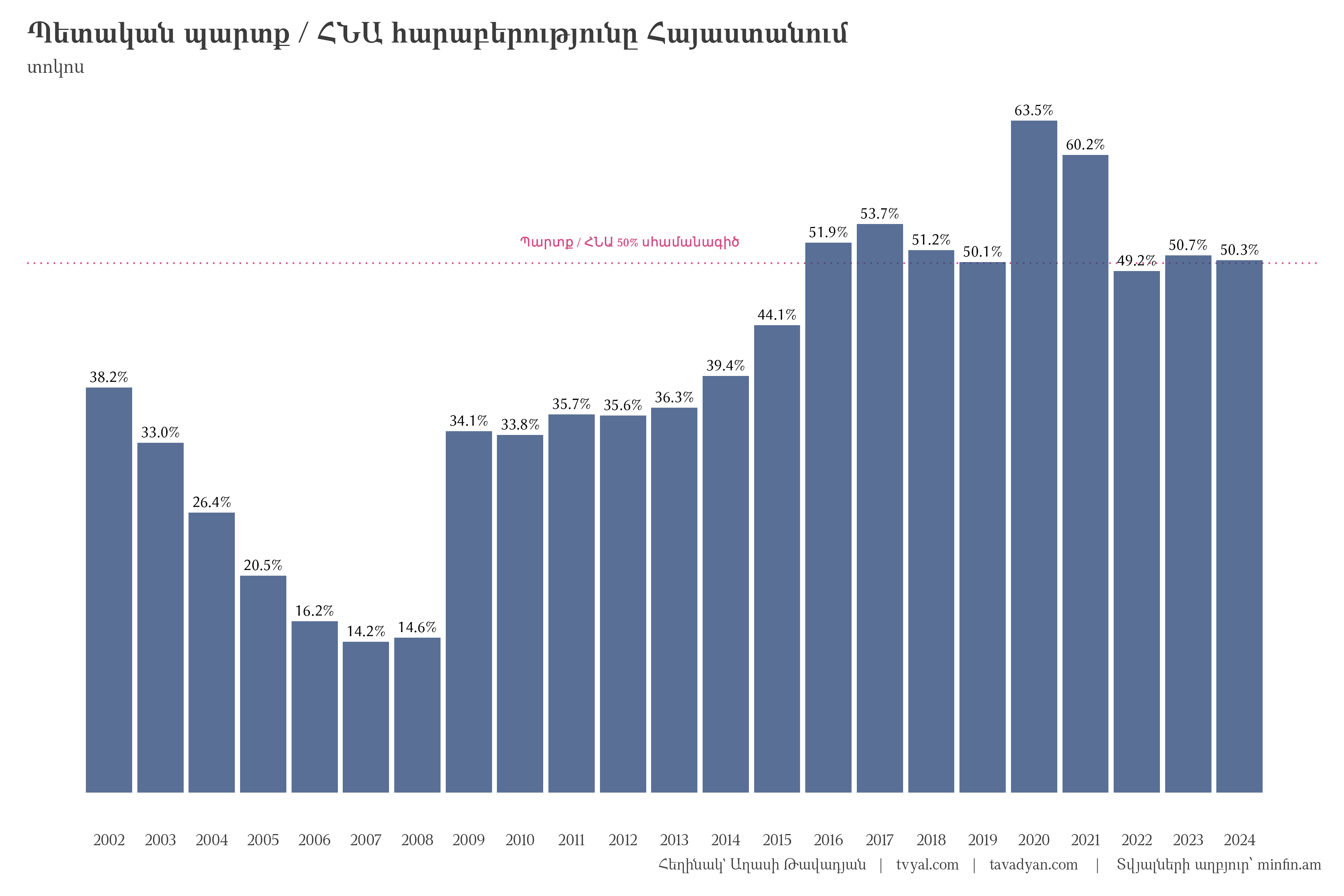

Approaching the danger line:

debt/GDP ratio at the 50% threshold

Chart 3.

One of the most important indicators for any country is the ratio of public debt to GDP, which is currently around 50% in Armenia. This is a danger zone because under the EAEU agreement, we are obligated not to keep this indicator above 50%. Moreover, under Armenian legislation, if the debt/GDP ratio crosses the 60% threshold, the government must immediately start cutting expenses. Cement: TODO: explain in the terms of a family which depth is bigger then half of their income (or product), if it is so this can be dangerous as the burdon of interest payments will pe put on the future generations. Interestingly, there have already been historical instances of crossing this threshold. In 2016, the debt/GDP ratio reached 51.9%, and in 2020-21 (due to the coronavirus and the war), the indicator rose to 63.5%. In certain quarters, it even reached 69.8%.

The truth hidden behind the “leapfrog” growth

The authorities often boast of “dazzling” economic indicators. For example, in 2024, Armenia’s exports recorded a 52% growth, reaching $13.1 billion. However, behind this number lies an important reality: 61.4% of the exports was gold re-exported from Russia to other countries through Armenia. This phenomenon is strictly short-term and does not reflect the real state of the economy. The fact is that our “real” exports have decreased: by 11% to the EAEU, and by 14% to the EU.

The same picture applies to the 5.9% official growth. About 25% of this growth was provided by trade, which actually grew slower in 2024 than in previous years. The second largest contributor was the real estate sector (the rise in rental value of apartments), but there is already stagnation in this market: prices have fallen in both rental and buying/selling cases.

The mining and manufacturing sectors experienced a decline. Under such conditions, the only sectors recording stable growth have been the banking system and construction.

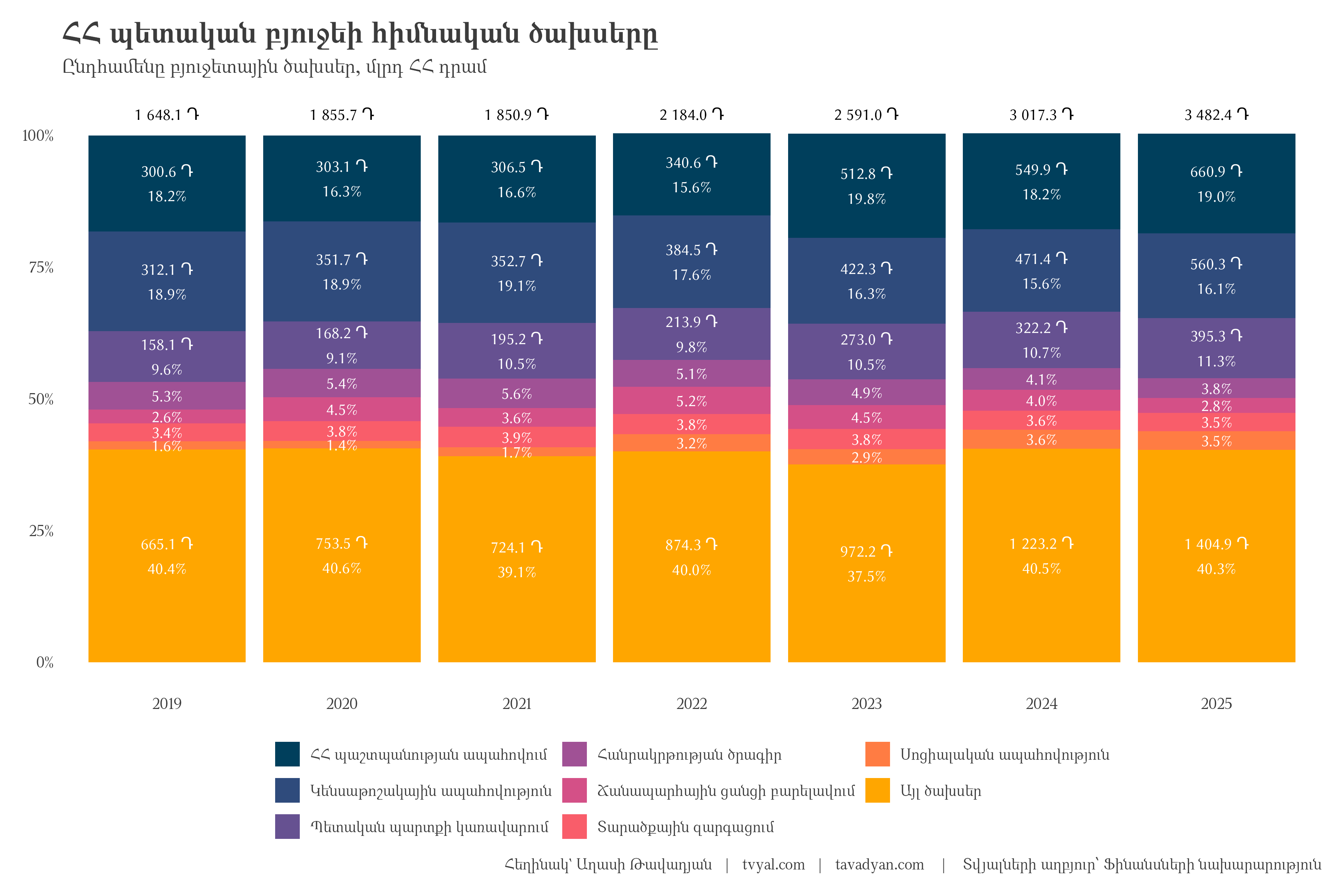

The third largest budget expense: debt servicing

Chart 4.

Recently, a misconception spread that the servicing of public debt is already in 3rd place among state budget expenditures and will soon become the second largest item, surpassing even pension insurance expenses. It is certainly true and concerning that a $750 million bond was issued at a high interest rate, but this cannot cause significant risks in the banking system. This is an incomplete understanding of budget expenditures. Of course, in 2025 it is planned that public debt management expenses will amount to a significant 11.3% of the budget or 395.3 billion drams. However, this has its reasons. Despite these large numbers, it should be noted that debt servicing has been kept within 9-11% of the budget in recent years; it has not become the biggest problem of the budget, as it is sometimes presented. It is true that public debt servicing has increased significantly and already has a certain degree of risk, but, as depicted in the fourth chart, it has always been in third place in recent years, occupying 9-11% of budget expenditures. The growth of public debt servicing in the budget is mainly due to the fact that the debt in Armenian drams already exceeds more than half of the total debt, which mitigates the risks arising from sharp exchange rate fluctuations in the long term, but increases the servicing fee in the short term, because interest rates on public debt in drams are higher than in dollars. However, the main reason is the significant gap in the 2024 budget, which is serviced by public debt. It is not expected that public debt servicing payments will exceed pension expenses in budget expenditures, and it is not expected that this will have a significant negative impact on the banking system or deposits, as the banking system is perhaps the only stable sector in Armenia. In 2025, what is the money generated from our taxes spent on? In first place are military expenses, in second are social expenses, and in third place is public debt servicing. 11.3% of the budget or 395.3 billion drams is spent on this last item. Interestingly, in 2019, the debt servicing expense was 158.1 billion drams, which means it has more than doubled in 7 years. This is mainly related to the change in the debt structure: the growth of dram debt, although protecting us from foreign exchange fluctuations, sits more expensively on the budget.

The impact of the exchange rate on public debt and GDP growth

The last chart clearly shows the impact of the dollar exchange rate on public debt servicing and, as a consequence, on the public debt/GDP ratio. The more the dram appreciates against the dollar, the cheaper public debt servicing becomes, therefore the public debt/GDP ratio decreases, and conversely, the more the dram depreciates, the more the public debt/GDP ratio tends to grow.

Chart 5.

It should be noted that since 2020, the Armenian dram is the most appreciated among convertible currencies, which negatively affects real exports, as well as tourism and the IT sector. This exerts some pressure on the dram, which is virtually soft-pegged to the dollar. The depreciation of the dram will negatively affect public debt servicing and, as a secondary consequence, GDP growth. The chart also shows the inverse relationship between public debt/GDP growth. In the case of negative GDP growth, public debt increases sharply because the target set by the state budget is not met with negative GDP growth, resulting in the forced consumption of the budget reserve fund and subsequently an increase in public debt. This trend is visible in the last chart in 2010, after an average 12 percent economic growth from 2002-2008. This decline was due to the Global Financial Crisis. A similar situation was also observed in 2020; the economic decline, this time, was due to another global phenomenon: the COVID-19 pandemic. As a result, both crises increased the public debt/GDP ratio. In other words, the dram exchange rate has a direct impact on the growth of public debt, while GDP growth has an inverse impact. Over the past 25 years, negative GDP growth has mainly been due to global “black swan” events.

2025: a difficult year for the economy

The current economic situation has pros and cons that must be considered during 2025:

What is good?

- More than half of the debt is internal, which protects us from foreign exchange fluctuations.

- Almost half of the debt (49%) is in drams, which reduces the potential negative impact of the dollar’s depreciation.

What to worry about?

- The debt/GDP ratio (around 50%) has already reached the maximum threshold set by the EAEU.

- In 2024, our “real” exports (excluding gold) decreased.

- There is a gap in the budget; taxes were under-collected by 8%.

- The real estate market, which had contributed to economic growth, is now stagnant.

- In 2025, a sharp decrease in gold re-exports is expected, which could lead to a nearly 30% reduction in total exports (from $13.1 billion to $9 billion).

All this shows that 2025 will be a difficult year for the Armenian economy. Gold export transactions have hidden the real state of the economy, and now this reality must be faced. This is a potential risk regarding the underperformance of the 2025 budget, which as a result could widen the budget gap and subsequently increase new public debt. This risk must be taken into account.

Now it is no longer possible to sharply increase debt to stimulate the economy. At this moment, when Armenia is at a critical point, greater attention must be paid to cost efficiency and the development of a balanced public debt management strategy.

First of all, one must think about cost efficiency and reduction, because continuing to spend at the same pace by borrowing is quite dangerous.

2025 will be full of challenges for the Armenian economy. The situation is still manageable, but requires a very cautious approach, especially in public debt management.

Overall, one must think about increasing the efficiency of budget expenditures and, as a result, lowering the public debt / GDP ratio, which will increase the economic cushion in the future in the event of global economic shocks.